About the CoMSES Model Library more info

Our mission is to help computational modelers at all levels engage in the establishment and adoption of community standards and good practices for developing and sharing computational models. Model authors can freely publish their model source code in the Computational Model Library alongside narrative documentation, open science metadata, and other emerging open science norms that facilitate software citation, reproducibility, interoperability, and reuse. Model authors can also request peer review of their computational models to receive a DOI.

All users of models published in the library must cite model authors when they use and benefit from their code.

Please check out our model publishing tutorial and contact us if you have any questions or concerns about publishing your model(s) in the Computational Model Library.

We also maintain a curated database of over 7500 publications of agent-based and individual based models with additional detailed metadata on availability of code and bibliometric information on the landscape of ABM/IBM publications that we welcome you to explore.

Displaying 4 of 4 results financial markets clear search

Peer reviewed A financial market with zero intelligence agents

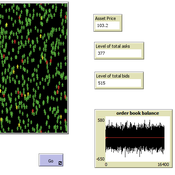

edgarkp | Published Wednesday, March 27, 2024The model’s aim is to represent the price dynamics under very simple market conditions, given the values adopted by the user for the model parameters. We suppose the market of a financial asset contains agents on the hypothesis they have zero-intelligence. In each period, a certain amount of agents are randomly selected to participate to the market. Each of these agents decides, in a equiprobable way, between proposing to make a transaction (talk = 1) or not (talk = 0). Again in an equiprobable way, each participating agent decides to speak on the supply (ask) or the demand side (bid) of the market, and proposes a volume of assets, where this number is drawn randomly from a uniform distribution. The granularity depends on various factors, including market conventions, the type of assets or goods being traded, and regulatory requirements. In some markets, high granularity is essential to capture small price movements accurately, while in others, coarser granularity is sufficient due to the nature of the assets or goods being traded

Portfolio Optimization and Trading Strategies: a simulation approach

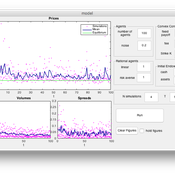

Alessio Emanuele Biondo Laura Mazzarino | Published Sunday, March 20, 2022This model analyzes two investors forming their expectations with heterogeneous strategies in order to optimize their portfolios by means of a Sharpe ratio maximization. Traders are distinguished according to their methodology used in forecasting. Two acknowledged algorithms of technical analysis have been implemented to compare portfolios performances and assess profitability of each technique.

Multi Asset Variable Network Stock Market Model

Matthew Oldham | Published Monday, September 12, 2016 | Last modified Tuesday, October 10, 2017An artifcal stock market model that allows users to vary the number of risky assets as well as the network topology that investors forms in an attempt to understand the dynamics of the market.

An Agent Based Model for implementing a double auction financial market

Annalisa Fabretti | Published Thursday, April 14, 2016The model implements a double auction financial markets with two types of agents: rational and noise. The model aims to study the impact of different compensation structure on the market stability and market quantities as prices, volumes, spreads.